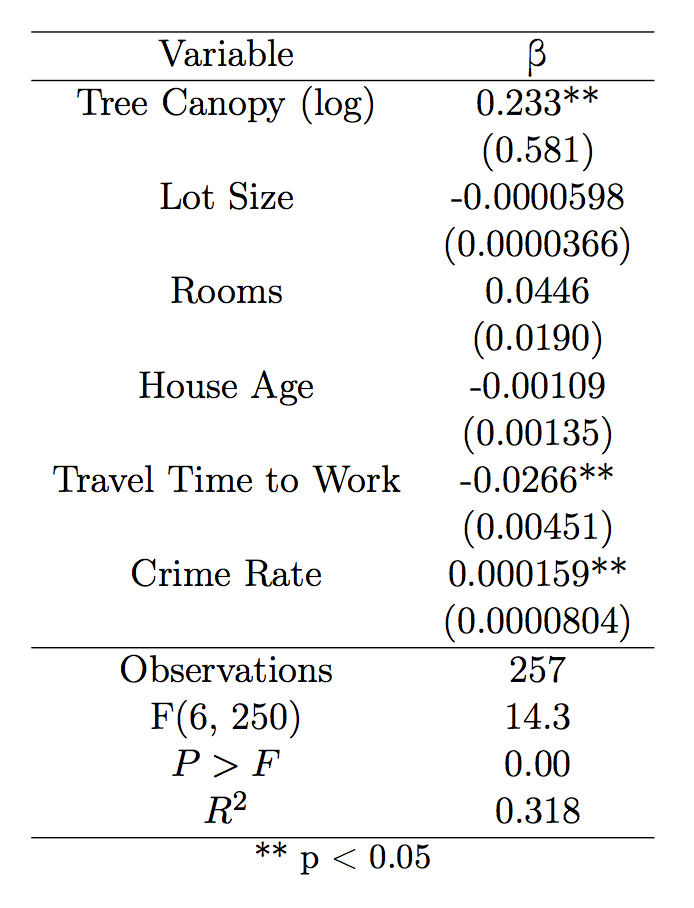

The first regression measured house price as a function of Tree Canopy, controlling for structural characteristics of the house as well as neighborhood characteristics. Here, the included structural characteristics are lot size, number of rooms, and house age. The included neighborhood characteristics are travel time to work and local crime rate. The regression employs robust standard errors to account for possible heteroskedasticity in the model. The results are summarized in the following table.

This regression, notably, shows a significant effect of Tree Canopy upon house price. The coefficient is substantive, indicating that a 1% increase in tree canopy is associated with a 0.233% increase in housing price. At four standard errors from zero, it is also highly significant. These values are substantial, which may be a result of endogeneity due to omitted variables. Though I attempted to include the most important variables, there are certainly a wealth of other measurable structural and neighborhood characteristics that could be included. It is also certainly possible, however, that the observed implicit price of tree canopy is simply larger than expected.

Taking the results at face value, we can determine the implicit price for tree canopy in the statistically average block group. This hypothetical block group has a median house value of $351,000 and a tree canopy proportion of 0.25. Therefore, a 1% increase in tree canopy would add 0.025 to the tree canopy proportion, and increase housing prices by $817.83. This number is high, but not out of line with estimates from previous literature. Recall that Payne estimated that the addition of 29 trees to a half-acre property increased prices by $4,300. Morales’ 1980 paper found that “good tree cover” added 6% to values for a total increase of $2,686, and Anderson and Cordell found that landscaping including trees added up to $3,073 to house value in 1985. Although none of these papers deal with percent increases to tree canopy, we should also note that none of these values are inflation-adjusted to compare to 2015. For example, Payne’s estimate of a $4,300 increase in value is comparable to $23,700 in 2015 dollars.

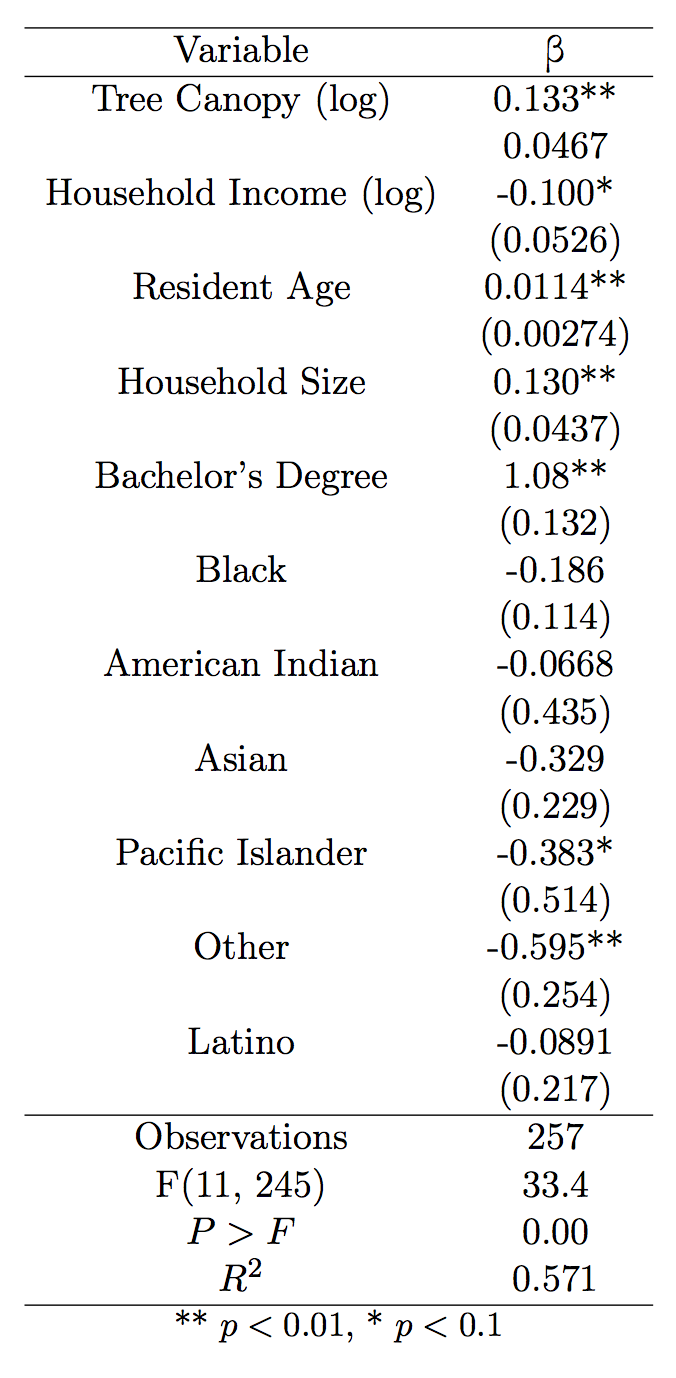

Having determined an overall implicit elasticity for Portland, I then constructed a variable for willingness-to-pay from the product of the Tree Canopy (log) coefficient and House Price. I logged this variable and regressed it against demographic characteristics of the residents in each block group. The results are summarized in the following table.

This table reports how willingness-to-pay for tree canopy varies with characteristics of the residents. The first five characteristics are most notable. All have a significant relationship with WTP—Age, Size, and Bachelor’s Degree at the 1% level, Median Household Income at the 6% level. At these levels, a 1-year increase in average resident age would yield a 0.0114\% increase in WTP, a 1-resident increase in average household size would yield a 0.130% increase in WTP, and a 0.01 increase in the proportion of residents with a bachelor’s degree would yield a 1.08% increase in WTP. These results indicate that a prospective increase in tree canopy would generate the greatest welfare gains in a neighborhood with older residents, larger household sizes, and a higher proportion of residents with a college education.

Income is also a significant determinant of WTP, but its results are somewhat counterintuitive. The coefficient is negative, indicating that a 1% increase in income would yield a 0.0998% decrease in WTP. This is unlikely to represent the reality of the situation, and it is more reasonable to assume that this results from endogeneity in the model. In this case, there is most likely an omitted variable with is correlated with income, willingness-to-pay, and the error term. It is certainly a jumping-off point for improvement to the model.

Nevertheless, these results do much to explain the value of tree canopy to a residential area. The presence of tree canopy is apparently valued substantively by current and prospective homeowners, and contributes as such to the housing market. Note that, as the title of this paper implies, this valuation misses any public value of urban canopy—anything not reflected in the price of housing does not show up in this analysis. Nevertheless, it is reasonable to assume that tree canopy may also have value as a public good—a topic worth further study.